LOCATION, LOCATION

Molony's comments bring up a crucial point about housing prices. National data may be interesting, but it's not very helpful for planners advising clients who want to buy or sell a house on a specific lot. Lately housing price movements have varied enormously from place to place. The chart, "Regional Differences," on page 76, shows NAR's regional data on median sales prices of existing single-family homes.

As these numbers show, price declines in the western states over the last two years have been far steeper than in other regions of the United States, reflecting the huge boom in certain markets in previous years. Prices in the West plummeted 37% from 2007 through 2009. In many areas of the South and Midwest, however, prices did not go through a boom and bust in the early years of this century, so they may already be at or near the bottom of this cycle. Prices in the South fell 13.3% over the last two years, while prices in the Midwest were only down 11.5%

The shadow inventory threat will be most ominous in the areas with the greatest portion of distressed homeowners. RealtyTrac reports that California and Florida alone accounted for about 37% of all national foreclosure filings in August 2010. In areas with less speculative building and fewer distressed homeowners, the shadow cast by future housing supply might not be as long.

BALANCING ACT

The question is whether today's buyers should wait, for fear that shadow inventory will drag down prices even further in the next few years. Yun points to a hopeful indicator on the supply side.

"One aspect of the shadow inventory that people aren't talking about is the lack of inventory of newly constructed homes," he says. In a normal year, Yun explains, there is always a flow of new homes hitting the market that needs to be absorbed. But in today's market, the low level of housing starts has cut off the normal flow of new home inventory. "So the low number of new homes will help offset shadow inventory, providing some help in the overall inventory picture."

Luschini concurs that weak housing starts are good news for home prices. "We don't need more inventory now."

What's more, it may be unrealistic to expect millions of homes will be dumped on the market in the next few years, driving down prices. Lenders who find themselves overstocked with real estate-owned (REO) property are being cautious. "On the front end, seriously delinquent loans are rolling into foreclosure at an unusually slow rate," Saccacio says. "On the back-end, the dammed-up inventory of properties already in foreclosure is moving to REO in a steady stream rather than a flood-presumably to prevent further erosion of home prices."

Luschini also sees evidence of efforts to keep housing supply and demand on an even keel. "Many homes are owned by banks, ready to come back on the market," he says. "Banks don't want to be in the business of owning homes. At the same time, they are reluctant to bring too many homes to the market, for fear of exacerbating weakness in home prices."

Thus lenders may be both reluctant home owners and reluctant home sellers. "We see a tug-of-war," Luschini explains. "As the economic recovery continues, more homes will come to market from banks and other owners. This increased supply will keep prices down." On the other end of the rope, when excess supply threatens to pull prices down, banks may rein in the supply of foreclosed properties so that prices can firm up. Arnott agrees that such activity is "clearly going on" and will put a damper on housing prices.

Luschini concludes that home prices are likely to stay "flattish" for several years. The inventory will find its way onto the market, and there will be some continued softness. "Home prices might drop 5% or so, nationwide, but the price drops won't be anything like we've seen in the past few years," he predicts, adding that because the housing market is highly regionalized, some areas of the country may see higher prices while others suffer steeper drops.

What might put housing prices on solid footing? "The answer to price stability is more jobs," Luschini says "When more people are working, more people will be able to commit to service the debt that comes with home ownership." With unemployment still well over 9%, it may be awhile before housing prices can resume an upward surge. In the meantime, the national housing price indexes mighty not stray far from current levels as lenders expand and contract the supply of REO properties coming onto the market.

How might a foreclosure moratorium affect housing prices? In the short term, it could stem further housing price declines because it would preclude new inventory from hitting the market, according to Luschini.

In the longer term, supply will surge once the moratorium is lifted, and prices will fall, says Feifei Li, director of research at Research Affiliates. "The moratorium won't make troubled homes disappear. They will hit the market eventually and cause a big spike in supply, driving prices down further."

By Donald Jay Korn

Catch the conclusion in Part 4 tomorrow!

Miss Part 1 or Part 2? Read them now!

Showing posts with label housing market. Show all posts

Showing posts with label housing market. Show all posts

Wednesday, November 3, 2010

Thursday, July 29, 2010

What's Driving the Sale of Downtown Luxury Condos?

By Dennis Rodkin, Chicago Magazine

In the first few months of 2010, as some local developers slashed prices or staged auctions on their newly built condominiums, a small segment at the upper end of the condo market flourished. As Gail Lissner of Appraisal Research Counselors notes, “There are always wealthy people with the ability to buy.” The big difference lately is that those well-heeled folks have been shelling out princely sums to buy luxurious new condos in downtown high-rises. “These are not speculators buying cookie-cutter condos,” says Lissner. “By and large, they are buying to live in these really high-end, unique places.”

Consider these numbers: From the beginning of the year until the middle of May, about 40 downtown condos have been sold for $2 million or more—and most of those condos were in buildings that opened in the last two years. (Some sales may have not yet appeared in public records.) They ranged from an $8.182-million sale at the Elysian—the 60-story tower at 11 East Walton Street designed by Lucien Lagrange—to a three-bedroom unit that went for a little more than $2.24 million at Aqua, the much-praised skyscraper at 225 North Columbus Drive that Jeanne Gang designed for Magellan Development. (The Elysian sale was the highest price paid for a Chicago condo since November 2006, when a 61st-floor unit at the Park Tower—at 800 North Michigan Avenue—went for $8.275 million.)

What’s driving the sales? To update an old real-estate adage: timing, timing, timing. Many of these new elite homeowners made their decision to buy several years ago, while buildings were under construction or still in the planning stage—and before the recession punctured the real-estate boom. With those condo towers now ready for residents, the folks who agreed years ago to buy are finally inking the deals.

That’s generally what’s been happening at the Elysian, according to Caryl Dillon, who was the tower’s sales agent. Since January 1st, at least 16 buyers there closed on condos priced at $2 million or more (in addition to the $8.182-million sale already mentioned, one condo went for $7.25 million and another for $6.9 million). That’s on top of a first round of December 2009 closings at $2 million and up. Meanwhile, at The Legacy (which recently opened at 60 East Monroe Street), three units priced at more than $2 million were among the first closings in the building—and usually the earliest buyers sign off on the earliest closings. (Since condos on a building’s bottom floors are often finished first, some lower-level, lower-priced units bought during construction can also be among the earliest closings.)

Buyers who signed contracts before the bust could have opted to cancel their contracts when the economy soured—as did numerous buyers of medium-priced homes. But “10 percent [the standard deposit on a condo] is a lot to walk away from” on a multimillion-dollar sale, Lissner says. Still, as she suggests, it’s also likely that for many of these rich buyers “their lifestyle hasn’t changed in the downturn.”

Janet Owen, a Sudler Sotheby’s International agent who works exclusively in the luxury market, points out that many rich people have not had to worry about the tight mortgage-financing climate that has contributed to the drag on the larger real-estate market. Mortgage lenders have been requiring bigger down payments, higher credit scores, and more detailed documentation of financial histories from average buyers. “These aren’t issues [wealthy potential homeowners] have to think about,” says Owen. On top of this, she notes, “their buying had nothing to do with the $8,000 federal tax credit.”

That is especially true of well-to-do buyers who made their purchase decisions recently. In early May, someone paid $2.3 million for a previously owned condo on the 51st floor of the Trump International Hotel & Tower (that building, at 401 North Wabash Avenue, opened in 2008). Another buyer spent $3.45 million in April for a 54th–floor condo at 55 East Erie that an investor had held on to since 2003. These new purchasers “are almost always cash buyers,” says Tere Proctor, who was the director of sales at Trump before returning to agency work (at Koenig & Strey Real Living). “They see the value in buildings like Trump and the Elysian, and they’re banking on knowing that whenever the market gets better, they will be holding valuable real estate.”

Read the full article and see building highlights here.

In the first few months of 2010, as some local developers slashed prices or staged auctions on their newly built condominiums, a small segment at the upper end of the condo market flourished. As Gail Lissner of Appraisal Research Counselors notes, “There are always wealthy people with the ability to buy.” The big difference lately is that those well-heeled folks have been shelling out princely sums to buy luxurious new condos in downtown high-rises. “These are not speculators buying cookie-cutter condos,” says Lissner. “By and large, they are buying to live in these really high-end, unique places.”

Consider these numbers: From the beginning of the year until the middle of May, about 40 downtown condos have been sold for $2 million or more—and most of those condos were in buildings that opened in the last two years. (Some sales may have not yet appeared in public records.) They ranged from an $8.182-million sale at the Elysian—the 60-story tower at 11 East Walton Street designed by Lucien Lagrange—to a three-bedroom unit that went for a little more than $2.24 million at Aqua, the much-praised skyscraper at 225 North Columbus Drive that Jeanne Gang designed for Magellan Development. (The Elysian sale was the highest price paid for a Chicago condo since November 2006, when a 61st-floor unit at the Park Tower—at 800 North Michigan Avenue—went for $8.275 million.)

What’s driving the sales? To update an old real-estate adage: timing, timing, timing. Many of these new elite homeowners made their decision to buy several years ago, while buildings were under construction or still in the planning stage—and before the recession punctured the real-estate boom. With those condo towers now ready for residents, the folks who agreed years ago to buy are finally inking the deals.

That’s generally what’s been happening at the Elysian, according to Caryl Dillon, who was the tower’s sales agent. Since January 1st, at least 16 buyers there closed on condos priced at $2 million or more (in addition to the $8.182-million sale already mentioned, one condo went for $7.25 million and another for $6.9 million). That’s on top of a first round of December 2009 closings at $2 million and up. Meanwhile, at The Legacy (which recently opened at 60 East Monroe Street), three units priced at more than $2 million were among the first closings in the building—and usually the earliest buyers sign off on the earliest closings. (Since condos on a building’s bottom floors are often finished first, some lower-level, lower-priced units bought during construction can also be among the earliest closings.)

Buyers who signed contracts before the bust could have opted to cancel their contracts when the economy soured—as did numerous buyers of medium-priced homes. But “10 percent [the standard deposit on a condo] is a lot to walk away from” on a multimillion-dollar sale, Lissner says. Still, as she suggests, it’s also likely that for many of these rich buyers “their lifestyle hasn’t changed in the downturn.”

Janet Owen, a Sudler Sotheby’s International agent who works exclusively in the luxury market, points out that many rich people have not had to worry about the tight mortgage-financing climate that has contributed to the drag on the larger real-estate market. Mortgage lenders have been requiring bigger down payments, higher credit scores, and more detailed documentation of financial histories from average buyers. “These aren’t issues [wealthy potential homeowners] have to think about,” says Owen. On top of this, she notes, “their buying had nothing to do with the $8,000 federal tax credit.”

That is especially true of well-to-do buyers who made their purchase decisions recently. In early May, someone paid $2.3 million for a previously owned condo on the 51st floor of the Trump International Hotel & Tower (that building, at 401 North Wabash Avenue, opened in 2008). Another buyer spent $3.45 million in April for a 54th–floor condo at 55 East Erie that an investor had held on to since 2003. These new purchasers “are almost always cash buyers,” says Tere Proctor, who was the director of sales at Trump before returning to agency work (at Koenig & Strey Real Living). “They see the value in buildings like Trump and the Elysian, and they’re banking on knowing that whenever the market gets better, they will be holding valuable real estate.”

Read the full article and see building highlights here.

Wednesday, July 28, 2010

Home Affordability is the best it has been in decades!

Daniel Kelley is the lead real estate analyst and portfolio manager of the Fidelity Select Construction and Housing Portfolio.

"Having just gone through a potentially once-in-a-lifetime down market, there is a bright light. Home affordability is the best in decades. In fact, on average, today's homebuyers have the lowest mortgage payments as a percentage of income in 30 years," wrote Kelley in a recent research report.

"Having just gone through a potentially once-in-a-lifetime down market, there is a bright light. Home affordability is the best in decades. In fact, on average, today's homebuyers have the lowest mortgage payments as a percentage of income in 30 years," wrote Kelley in a recent research report.

Thursday, July 8, 2010

CATERING TO SENIORS CAN MAKE YOUR BUSINESS BOOM

Even when business isn’t booming, there are still plenty of opportunities to enter the senior market, especially since baby boomers often seek a simpler way of life regardless of the push or pull of market forces. Boomers are an ever-growing market segment, and they are more active and picky than the 50+ buyers in the past. Whether you’ve been working in the senior market for ages or are just looking to discover its hidden potential, you must understand how to cater to boomers’ needs to tap into a market that may lead you to new success.

Taking the Additional Time to Make a Senior Sale

To meet seniors’ long-term needs, agents and developers say selling to baby boomers often takes longer than selling to younger clients. Lucchetti notes the emotional attachment seniors have to their homes – some of which they have lived in for a lifetime – often leads to a longer lead time before they make the final move.

Hartz notes that senior buyers are often cautious and conservative – particularly in this market. However, they often move quickly when they sell their property as they are ready for the next step in their life and can be cash buyers – a huge plus in any market.

Since the sale can take longer with boomers, agents must be persistent in their communication with clients. Thompson uses newsletters and community outreach to stay in contact with seniors, while communicating with their relatives through e-mail. She says you must build a relationship over time to gain their trust, which requires you to stay in touch with them frequently.

Just because these clients are more mature, it doesn’t mean they are still living in the dark ages. Tricia Fox of Keller Williams Luxury Homes says she e-mails back and forth with most baby boomer clients, and occasionally texts with those savvy enough to do so. Find out which method of communication works best for the client, and proceed accordingly.

“Knowing the effects that arthritis, as well as loss of hearing and vision, can have on communication and decision making has a big impact on how you deal with boomers and other seniors,” says Kunicki.

How You Can Benefit from Boomer Business

Despite all the additional work required, Fox says the senior market is the “best market” to be in at the moment, as many seniors are buying a second home or downsizing and embracing the Chicago area.

While it is not always true, oftentimes boomers are the ones out there with money to spend. Boomer Project founder/president Matt Thornhill claims that the over-50 crowd outspends the under-50 crowd by $400 billion. Additionally, the latest survey conducted by ProMatura Group found that 50+ sentiment is on the rise, and that 50+ primary home purchases have risen by 5 percent. With more years in the workforce, boomers have the potential to spend a lot more money on their next step in life.

With Social Security no longer a primary source of income for many boomers, there is a growing trend of delaying retirement. The Del Webb survey found that boomers turning 50 this year plan to retire a median of four years later than 50 year olds in 1996, at age 67 versus 63. Among the younger boomers, 72 percent plan to work in some fashion during their retirement years. With more and more seniors continuing to work and putting off retirement, many are no longer interested in communities that are far from employment opportunities.

When it comes to the bottom line, most agents claim the commission in the senior market is comparable to the pre-retirement age market. Additionally, some independent senior communities offering rental properties, such as LaGrange Pointe in LaGrange, provide commission to agents.

Overall, boomers and seniors are not a market to be ignored. The U.S. Census states that the over-50 crowd will grow 21 percent in size in 10 years, while the 18 to 49 population will remain the same size. As the number increases, so do your opportunities to find additional clients – and sales. Those who cater to the senior market may find that their business grows on all fronts, if they take the time to understand the specific and changing needs of baby boomers and their families.

For the full article click here.

Morgan Phelps, Chicago Agent Magazine

Taking the Additional Time to Make a Senior Sale

To meet seniors’ long-term needs, agents and developers say selling to baby boomers often takes longer than selling to younger clients. Lucchetti notes the emotional attachment seniors have to their homes – some of which they have lived in for a lifetime – often leads to a longer lead time before they make the final move.

Hartz notes that senior buyers are often cautious and conservative – particularly in this market. However, they often move quickly when they sell their property as they are ready for the next step in their life and can be cash buyers – a huge plus in any market.

Since the sale can take longer with boomers, agents must be persistent in their communication with clients. Thompson uses newsletters and community outreach to stay in contact with seniors, while communicating with their relatives through e-mail. She says you must build a relationship over time to gain their trust, which requires you to stay in touch with them frequently.

Just because these clients are more mature, it doesn’t mean they are still living in the dark ages. Tricia Fox of Keller Williams Luxury Homes says she e-mails back and forth with most baby boomer clients, and occasionally texts with those savvy enough to do so. Find out which method of communication works best for the client, and proceed accordingly.

“Knowing the effects that arthritis, as well as loss of hearing and vision, can have on communication and decision making has a big impact on how you deal with boomers and other seniors,” says Kunicki.

How You Can Benefit from Boomer Business

Despite all the additional work required, Fox says the senior market is the “best market” to be in at the moment, as many seniors are buying a second home or downsizing and embracing the Chicago area.

While it is not always true, oftentimes boomers are the ones out there with money to spend. Boomer Project founder/president Matt Thornhill claims that the over-50 crowd outspends the under-50 crowd by $400 billion. Additionally, the latest survey conducted by ProMatura Group found that 50+ sentiment is on the rise, and that 50+ primary home purchases have risen by 5 percent. With more years in the workforce, boomers have the potential to spend a lot more money on their next step in life.

With Social Security no longer a primary source of income for many boomers, there is a growing trend of delaying retirement. The Del Webb survey found that boomers turning 50 this year plan to retire a median of four years later than 50 year olds in 1996, at age 67 versus 63. Among the younger boomers, 72 percent plan to work in some fashion during their retirement years. With more and more seniors continuing to work and putting off retirement, many are no longer interested in communities that are far from employment opportunities.

When it comes to the bottom line, most agents claim the commission in the senior market is comparable to the pre-retirement age market. Additionally, some independent senior communities offering rental properties, such as LaGrange Pointe in LaGrange, provide commission to agents.

Overall, boomers and seniors are not a market to be ignored. The U.S. Census states that the over-50 crowd will grow 21 percent in size in 10 years, while the 18 to 49 population will remain the same size. As the number increases, so do your opportunities to find additional clients – and sales. Those who cater to the senior market may find that their business grows on all fronts, if they take the time to understand the specific and changing needs of baby boomers and their families.

For the full article click here.

Morgan Phelps, Chicago Agent Magazine

Wednesday, July 7, 2010

YTD condo closings up 45% over 2009

In the first six months of this year, condo sales have dramatically increased compared to the first half of 2009. And June closings were up 26% over May.

According to figures generated for ChicagoCondosOnline.com by MRED, the regional MLS, year-to-date sales of Chicago condos through June 2010 are:

* Up 42% in total dollar volume, to $1.8 billion

* Up 45% in units closed, to 5,630

* Down 6% in median sales price, to $263,700

* Down 6% in average market time, to 148 days.

Comparing June sales to May:

* Units closed were up 26%, from 1,083 to 1,365 closings

* Dollar volume was up 27%, from $341 million to $434 million

* Median sales price was up 2%, from $264,900 to $270,000

* Average market time was flat, at 144 days

For details on month-over-month and year-over-year: click here.

For previous market reports: click here.

According to figures generated for ChicagoCondosOnline.com by MRED, the regional MLS, year-to-date sales of Chicago condos through June 2010 are:

* Up 42% in total dollar volume, to $1.8 billion

* Up 45% in units closed, to 5,630

* Down 6% in median sales price, to $263,700

* Down 6% in average market time, to 148 days.

Comparing June sales to May:

* Units closed were up 26%, from 1,083 to 1,365 closings

* Dollar volume was up 27%, from $341 million to $434 million

* Median sales price was up 2%, from $264,900 to $270,000

* Average market time was flat, at 144 days

For details on month-over-month and year-over-year: click here.

For previous market reports: click here.

Wednesday, June 30, 2010

Chicago Home Sales

Crain's reported today..

The Chicago-area index seemed to hit bottom in April 2009, after a 27.4% drop from its September 2006 peak. The index rose steadily through last September but then started falling again. It now stands 28.6% below its peak and roughly where it was in May 2002.

S&P also reported that an index of Chicago-area condominium prices rose 5.2% from March to April. The local condo index fell 6.7% on a year-over-year basis and was down 22.5% from its peak in September 2007.

The Chicago-area index seemed to hit bottom in April 2009, after a 27.4% drop from its September 2006 peak. The index rose steadily through last September but then started falling again. It now stands 28.6% below its peak and roughly where it was in May 2002.

S&P also reported that an index of Chicago-area condominium prices rose 5.2% from March to April. The local condo index fell 6.7% on a year-over-year basis and was down 22.5% from its peak in September 2007.

Tuesday, June 22, 2010

Chicago home sales jump 32% in May

By: Lorene Yue June 22, 2010, Chicago Business

(Crain's) — More homes were sold in Chicago in May than a year earlier, marking the ninth month in a row of year-over-year gains.

The Illinois Assn. of Realtors reported Tuesday that last month's sales of 2,057 single-family houses and condominiums represented a 32.1% increase from May 2009 sales. The median price also rose, up 2.2% to $230,000, from the same month last year.

The city's May sales uptick was also seen in the greater Chicago area, where 33.6% more homes were sold. The median price for those homes, however, fell, down 4.8% to $190,500.

Illinois home sales were up 27.1%. The median price of the 11,638 homes sold statewide last month was $157,00, a slight increase from the $156,000 median of May 2009.

The National Assn. of Realtors said Midwest home sales remained strong in May as the homebuyers tax credit drove sales nearly 22% higher than in May 2009. The credit called for offers to be made by April 30.

The data released Tuesday show 130,000 sales in the 11-state Midwest region in May. The median home price increased more than 2%, to $150,700.

Midwest sales again rose more than national ones. Nonseasonally adjusted figures show May home sales nationwide increased about 18% over last year.

The Associated Press-Re/Max Monthly Housing Report, which also was released Tuesday, showed home sales increasing in all but one of 12 major Midwestern cities tracked. Fargo, N.D., led the region with a 66% sales jump. Detroit reported the only sales decrease, a 15% drop.

For more information and a breakdown of Chicago area sales click here.

(Crain's) — More homes were sold in Chicago in May than a year earlier, marking the ninth month in a row of year-over-year gains.

The Illinois Assn. of Realtors reported Tuesday that last month's sales of 2,057 single-family houses and condominiums represented a 32.1% increase from May 2009 sales. The median price also rose, up 2.2% to $230,000, from the same month last year.

The city's May sales uptick was also seen in the greater Chicago area, where 33.6% more homes were sold. The median price for those homes, however, fell, down 4.8% to $190,500.

Illinois home sales were up 27.1%. The median price of the 11,638 homes sold statewide last month was $157,00, a slight increase from the $156,000 median of May 2009.

The National Assn. of Realtors said Midwest home sales remained strong in May as the homebuyers tax credit drove sales nearly 22% higher than in May 2009. The credit called for offers to be made by April 30.

The data released Tuesday show 130,000 sales in the 11-state Midwest region in May. The median home price increased more than 2%, to $150,700.

Midwest sales again rose more than national ones. Nonseasonally adjusted figures show May home sales nationwide increased about 18% over last year.

The Associated Press-Re/Max Monthly Housing Report, which also was released Tuesday, showed home sales increasing in all but one of 12 major Midwestern cities tracked. Fargo, N.D., led the region with a 66% sales jump. Detroit reported the only sales decrease, a 15% drop.

For more information and a breakdown of Chicago area sales click here.

Monday, May 17, 2010

Trader pays over $7.25 million for Elysian condo

By: Andrew Schroedter May 17, 2010

(Crain’s) — An options trader is taking a gamble on the Elysian Hotel & Private Residences, paying more than $7.25 million for a condominium in the Gold Coast skyscraper that he hopes to flip for more than $10 million.

Igor Chernomzav, a co-founder of Hard Eight Futures LLC, bought a 12,000-square-foot unit on the 56th and 57th floors of the 60-story tower at 11 E. Walton St., which also features a 188-room hotel, according to property records.

Mr. Chernomzav, 33, who paid cash for the five-bedroom, two-level condo, plans to remodel the unit and put it back on the market, according to Tricia Fox of residential real estate firm Keller Williams, which brokered the sale.

The asking price will be between $10 million and $11 million, Ms. Fox says.

This is the second unit Mr. Chernomzav has purchased in the Elysian, after paying a reported $8.18 million in March for a 52nd-floor unit, which he is also remodeling. Whether he also plans to flip that condo could not be determined.

A spokesman for Mr. Chernomzav declines to comment.

Mr. Chernomzav started Chicago-based Hard Eight in 2004, five years after earning a philosophy degree from Princeton University, according to his firm’s Web site. Originally from San Antonio, he began his career in 1999 as an options trader for Susquehanna Investment, part of suburban Philadelphia-based Susquehanna International Group LLP.

For his recent purchase in the Elysian, the entrepreneur bought a contract for a unit signed several years ago by a speculator represented by Ms. Fox. The identity of the speculator and how much Mr. Chernomzav paid for the contract could not be determined.

But Mr. Chernomzav is paying developer Elysian Worldwide 25% less than the speculator’s original asking price of $9.5 million for the unit, which features a 25-foot living room ceiling and 360-degree views.

Zaga Arsic, also of Keller Williams, represented Mr. Chernomzav.

The deal is a sign that the high-end market is improving as sellers cut prices, says Craig Hogan, managing broker of Keller’s Gold Coast office.

“If the price is right, people will come look,” he says.

Mr. Chernomzav has paid the highest prices for units in the Elysian, surpassing the $6.88 million that James McNulty, former CEO of the Chicago Mercantile Exchange, paid in January for a 7,400-square-foot condo on the project’s 37th floor, according to property records. Mr. McNulty didn’t return a call seeking comment.

Buyers have closed on 31 of the 51 residential condo units in the building, says developer David Pisor, who in November was forced to abandon a plan to also sell the 188 hotel units in the building.

Another 15 residential condos are under contract, says Mr. Pisor, president and CEO of Chicago-based Elysian Worldwide LLC, who adds that sales traffic has picked up in the last 45 days.

“It was pretty brutal there for a while,” he says.

(Crain’s) — An options trader is taking a gamble on the Elysian Hotel & Private Residences, paying more than $7.25 million for a condominium in the Gold Coast skyscraper that he hopes to flip for more than $10 million.

Igor Chernomzav, a co-founder of Hard Eight Futures LLC, bought a 12,000-square-foot unit on the 56th and 57th floors of the 60-story tower at 11 E. Walton St., which also features a 188-room hotel, according to property records.

Mr. Chernomzav, 33, who paid cash for the five-bedroom, two-level condo, plans to remodel the unit and put it back on the market, according to Tricia Fox of residential real estate firm Keller Williams, which brokered the sale.

The asking price will be between $10 million and $11 million, Ms. Fox says.

This is the second unit Mr. Chernomzav has purchased in the Elysian, after paying a reported $8.18 million in March for a 52nd-floor unit, which he is also remodeling. Whether he also plans to flip that condo could not be determined.

A spokesman for Mr. Chernomzav declines to comment.

Mr. Chernomzav started Chicago-based Hard Eight in 2004, five years after earning a philosophy degree from Princeton University, according to his firm’s Web site. Originally from San Antonio, he began his career in 1999 as an options trader for Susquehanna Investment, part of suburban Philadelphia-based Susquehanna International Group LLP.

For his recent purchase in the Elysian, the entrepreneur bought a contract for a unit signed several years ago by a speculator represented by Ms. Fox. The identity of the speculator and how much Mr. Chernomzav paid for the contract could not be determined.

But Mr. Chernomzav is paying developer Elysian Worldwide 25% less than the speculator’s original asking price of $9.5 million for the unit, which features a 25-foot living room ceiling and 360-degree views.

Zaga Arsic, also of Keller Williams, represented Mr. Chernomzav.

The deal is a sign that the high-end market is improving as sellers cut prices, says Craig Hogan, managing broker of Keller’s Gold Coast office.

“If the price is right, people will come look,” he says.

Mr. Chernomzav has paid the highest prices for units in the Elysian, surpassing the $6.88 million that James McNulty, former CEO of the Chicago Mercantile Exchange, paid in January for a 7,400-square-foot condo on the project’s 37th floor, according to property records. Mr. McNulty didn’t return a call seeking comment.

Buyers have closed on 31 of the 51 residential condo units in the building, says developer David Pisor, who in November was forced to abandon a plan to also sell the 188 hotel units in the building.

Another 15 residential condos are under contract, says Mr. Pisor, president and CEO of Chicago-based Elysian Worldwide LLC, who adds that sales traffic has picked up in the last 45 days.

“It was pretty brutal there for a while,” he says.

Spire developer closes sales office at NBC Tower

By: Eddie Baeb May 17, 2010

(Crain’s) — The Chicago Spire has closed its lavish sales office in NBC Tower after settling an eviction lawsuit filed last fall by its landlord over unpaid rent.

Spire developer Shelbourne Development Group reportedly spent about $10 million to build out the spacious sales center on the 18th floor of NBC Tower, 455 N. Cityfront Plaza Drive, while the landlord kicked in almost $350,000.

The sales center, which included a fully built-out model, overlooked the Spire’s site at 400 N. Lake Shore Drive, where construction of the twisting tower that would be North America's tallest building halted in late 2008.

The closing comes nine months after the owner of NBC Tower, a partnership controlled by the family of German billionaire Hugo Mann, filed an eviction suit in August, alleging that Shelbourne stopped paying rent in April 2009 and that the building was owed more than $316,000.

The two sides settled the case in February, after the landlord obtained a judgment for about $55,000, part of the unpaid rent, according to a March 4 court order. The settlement apparently paved the way for Shelbourne to surrender the space.

Dublin, Ireland-based Shelbourne closed the sales center over the weekend. sources say. The company will now make sales pitches for the proposed 150-story condominium tower at Shelbourne’s local business office on Wacker Drive, the Chicago Tribune reported Monday on its Web site.

A Shelbourne spokeswoman didn’t respond to a call or e-mail from Crain’s.

But the spokeswoman told the Tribune that Garrett Kelleher was “being smart" by closing the sales center. "If you're in a situation where things are slowing down, you need to consolidate and you need to be smart,” she said.

Attorney Scott Kenig, a partner in Chicago law firm Randall & Kenig LLP, which represents the Mann family partnership, declines to comment.

(Crain’s) — The Chicago Spire has closed its lavish sales office in NBC Tower after settling an eviction lawsuit filed last fall by its landlord over unpaid rent.

Spire developer Shelbourne Development Group reportedly spent about $10 million to build out the spacious sales center on the 18th floor of NBC Tower, 455 N. Cityfront Plaza Drive, while the landlord kicked in almost $350,000.

The sales center, which included a fully built-out model, overlooked the Spire’s site at 400 N. Lake Shore Drive, where construction of the twisting tower that would be North America's tallest building halted in late 2008.

The closing comes nine months after the owner of NBC Tower, a partnership controlled by the family of German billionaire Hugo Mann, filed an eviction suit in August, alleging that Shelbourne stopped paying rent in April 2009 and that the building was owed more than $316,000.

The two sides settled the case in February, after the landlord obtained a judgment for about $55,000, part of the unpaid rent, according to a March 4 court order. The settlement apparently paved the way for Shelbourne to surrender the space.

Dublin, Ireland-based Shelbourne closed the sales center over the weekend. sources say. The company will now make sales pitches for the proposed 150-story condominium tower at Shelbourne’s local business office on Wacker Drive, the Chicago Tribune reported Monday on its Web site.

A Shelbourne spokeswoman didn’t respond to a call or e-mail from Crain’s.

But the spokeswoman told the Tribune that Garrett Kelleher was “being smart" by closing the sales center. "If you're in a situation where things are slowing down, you need to consolidate and you need to be smart,” she said.

Attorney Scott Kenig, a partner in Chicago law firm Randall & Kenig LLP, which represents the Mann family partnership, declines to comment.

Tuesday, January 19, 2010

Real Estate Outlook: Strong Sales Predicted

By Kenneth R. Harney, Realty Times

Will housing outperform the overall economy in 2010 as we pull out of the Great Recession?

Nothing is absolute in the predictions business, but there are solid indications that, yes, housing is likely to rebound more energetically than the overall economy.

Here's why: Even the most bearish Wall Street analysts now concede that home sales are up in many areas from year-earlier levels -- sometimes by extraordinary percentages.

For example, MDA DataQuick reports that sales in the greater Phoenix market in November were 62 percent higher than the year before.

Prices either have bottomed out in dozens of these markets or are close to it. That's because the distressed sales component of local volume - short sales, REOs and foreclosures - has been declining slowly but steadily.

In his latest forecast, Jay Brinkmann, chief economist for the Mortgage Bankers Association, says both existing and new home sales will be higher in 2010 than in 2009 - and 2009 was better than 2008.

No question that a key part of the energy in housing will be the direct result of stimulus efforts by the federal government - especially the two tax credit programs -- that will push sales and even pricing through mid year.

The overall economy, on the other hand, according to Brinkmann, is likely only to grow slowly in the first half of 2010, and not really warm up until the second half.

The heavy anchor dragging on national economic growth -- and on housing demand -- will continue to be unemployment. Brinkmann says that "the time of job destruction is over" in this cycle - that is, the number of new layoffs and new unemployment insurance claims filings are trending down.

But we haven't yet moved into the next phase nationwide - that of "job creation," which may not begin until later in the year, he says, and may be a long, slow process.

The National Association of Realtors' chief economist, Lawrence Yun, sees a strong sales year ahead - up 20 percent over 2009. In some markets, he also expects to see a return to modest and sustained price increases - anywhere from two to five percent on average.

Will higher interest rates put a big dent in these projections? Many economists are forecasting 30 year rates in the upper 5 percent range later in the year.

Those higher rates won't help - but last week they headed in the opposite direction. Thirty year fixed rates averaged 5.1 percent and 15 year rates were half a point below that - both down slightly from the week before, according to the Mortgage Bankers' national survey.

Published: January 19, 2010

Will housing outperform the overall economy in 2010 as we pull out of the Great Recession?

Nothing is absolute in the predictions business, but there are solid indications that, yes, housing is likely to rebound more energetically than the overall economy.

Here's why: Even the most bearish Wall Street analysts now concede that home sales are up in many areas from year-earlier levels -- sometimes by extraordinary percentages.

For example, MDA DataQuick reports that sales in the greater Phoenix market in November were 62 percent higher than the year before.

Prices either have bottomed out in dozens of these markets or are close to it. That's because the distressed sales component of local volume - short sales, REOs and foreclosures - has been declining slowly but steadily.

In his latest forecast, Jay Brinkmann, chief economist for the Mortgage Bankers Association, says both existing and new home sales will be higher in 2010 than in 2009 - and 2009 was better than 2008.

No question that a key part of the energy in housing will be the direct result of stimulus efforts by the federal government - especially the two tax credit programs -- that will push sales and even pricing through mid year.

The overall economy, on the other hand, according to Brinkmann, is likely only to grow slowly in the first half of 2010, and not really warm up until the second half.

The heavy anchor dragging on national economic growth -- and on housing demand -- will continue to be unemployment. Brinkmann says that "the time of job destruction is over" in this cycle - that is, the number of new layoffs and new unemployment insurance claims filings are trending down.

But we haven't yet moved into the next phase nationwide - that of "job creation," which may not begin until later in the year, he says, and may be a long, slow process.

The National Association of Realtors' chief economist, Lawrence Yun, sees a strong sales year ahead - up 20 percent over 2009. In some markets, he also expects to see a return to modest and sustained price increases - anywhere from two to five percent on average.

Will higher interest rates put a big dent in these projections? Many economists are forecasting 30 year rates in the upper 5 percent range later in the year.

Those higher rates won't help - but last week they headed in the opposite direction. Thirty year fixed rates averaged 5.1 percent and 15 year rates were half a point below that - both down slightly from the week before, according to the Mortgage Bankers' national survey.

Published: January 19, 2010

Monday, January 4, 2010

Home Value Loss Now but Increased Pricing Expected in 2010

By Phoebe Chongchua, Realty Times

There’s bad news and good news coming out of the housing market. Forbes Magazine released study results by Local Market Monitor that showed the cities that lost the most value are concentrated in some areas of California, Florida, Nevada, and the Northeast.

These cities were impacted by local and national factors such as increased unemployment and the rising cost of housing which resulted in homebuyers gambling on the odds of whether they could afford long-term housing.

West Coast housing markets fared the worst, losing the most value—21.6 percent since their peak. Florida housing lost 31 percent, the Northeast lost an average of 8.6 percent, and the Midwest lost, on average, 5.6 percent. The top five cities to lose value in the West (most in California): in California--Merced, (-62.11 percent), Stockton (-54.29), Modesto (-52.42), Vallejo-Fairfield (-47.62), and in Nevada—Las Vegas-Paradise (-47.53) In the South, the top five cities to lose the most value are located in Florida: Port St. Lucie (-46.43), Cape Coral-Fort-Myers (-46.38), Naples-Marco Island (-43.63), Bradenton-Sarasota-Venice (-41.52), and Fort Lauderdale-Pompano Beach-Deerfield Beach (-39.93).

In the Northeast, the top five cities to lose value are: Providence-New Bedford, R.I. (-17.30), Worcester, Mass. (-16.17), Atlantic City, N.J. (-16.15), Poughkeepsie-Newburgh, N.Y. (-14.60), and Barnstable Town, Mass. (-14.48).

Moving to the Midwest, the top five cities to lose value are in Michigan: Detroit-Livonia (-30.66), Warren-Troy-Farmington Hills (-27.95), Flint (-27.47), Ann Arbor (-20.37), and Jackson (-17.30). Source: Forbes, Francesca, Levy (12/21/2009).

According to First American CoreLogic’s LoanPerformance Home Price Index, home prices are expected to fall another 4.2 percent in 45 of the largest housing markets before hitting bottom. The Press Release states that, “The declines will be driven primarily by the large levels of foreclosures in these areas. However, improvement in both levels of inventories and unemployment are projected to prevail in the spring of next year, resulting in an average year-over-year appreciation of just under one percent by October of 2010 for these metropolitan markets.

The report also stated that, “In August 2010, the index is projecting that 12-month appreciation for national home prices will be 4.6 percent and that home prices in two of the most depressed markets, California and Florida, will show gains in excess of 7 percent.” Cities that are projected to experience the strongest recovery in 2010 are primarily concentrated in the large urban areas of California: San Francisco (+5.7 percent), Los Angeles (+5 percent), San Diego (+4.7 percent) and Sacramento (+4.6 percent).

The report cautions that a large inventory of homes owned by banks but not yet on the market could affect the increased pricing progress. Mark Fleming, chief economist for First American CoreLogic stated in a December Press Release, "We are continuing to see improvements in the year-over-year home price change as prices have remained relatively stable since April. The additional government support for the housing market has stimulated demand and restricted supply in 2009.” However, Fleming, added, “How these government supports are removed in 2010 and the moderation of pending inventory and negative equity will be critical to the continued stability of the housing market.”

There’s bad news and good news coming out of the housing market. Forbes Magazine released study results by Local Market Monitor that showed the cities that lost the most value are concentrated in some areas of California, Florida, Nevada, and the Northeast.

These cities were impacted by local and national factors such as increased unemployment and the rising cost of housing which resulted in homebuyers gambling on the odds of whether they could afford long-term housing.

West Coast housing markets fared the worst, losing the most value—21.6 percent since their peak. Florida housing lost 31 percent, the Northeast lost an average of 8.6 percent, and the Midwest lost, on average, 5.6 percent. The top five cities to lose value in the West (most in California): in California--Merced, (-62.11 percent), Stockton (-54.29), Modesto (-52.42), Vallejo-Fairfield (-47.62), and in Nevada—Las Vegas-Paradise (-47.53) In the South, the top five cities to lose the most value are located in Florida: Port St. Lucie (-46.43), Cape Coral-Fort-Myers (-46.38), Naples-Marco Island (-43.63), Bradenton-Sarasota-Venice (-41.52), and Fort Lauderdale-Pompano Beach-Deerfield Beach (-39.93).

In the Northeast, the top five cities to lose value are: Providence-New Bedford, R.I. (-17.30), Worcester, Mass. (-16.17), Atlantic City, N.J. (-16.15), Poughkeepsie-Newburgh, N.Y. (-14.60), and Barnstable Town, Mass. (-14.48).

Moving to the Midwest, the top five cities to lose value are in Michigan: Detroit-Livonia (-30.66), Warren-Troy-Farmington Hills (-27.95), Flint (-27.47), Ann Arbor (-20.37), and Jackson (-17.30). Source: Forbes, Francesca, Levy (12/21/2009).

According to First American CoreLogic’s LoanPerformance Home Price Index, home prices are expected to fall another 4.2 percent in 45 of the largest housing markets before hitting bottom. The Press Release states that, “The declines will be driven primarily by the large levels of foreclosures in these areas. However, improvement in both levels of inventories and unemployment are projected to prevail in the spring of next year, resulting in an average year-over-year appreciation of just under one percent by October of 2010 for these metropolitan markets.

The report also stated that, “In August 2010, the index is projecting that 12-month appreciation for national home prices will be 4.6 percent and that home prices in two of the most depressed markets, California and Florida, will show gains in excess of 7 percent.” Cities that are projected to experience the strongest recovery in 2010 are primarily concentrated in the large urban areas of California: San Francisco (+5.7 percent), Los Angeles (+5 percent), San Diego (+4.7 percent) and Sacramento (+4.6 percent).

The report cautions that a large inventory of homes owned by banks but not yet on the market could affect the increased pricing progress. Mark Fleming, chief economist for First American CoreLogic stated in a December Press Release, "We are continuing to see improvements in the year-over-year home price change as prices have remained relatively stable since April. The additional government support for the housing market has stimulated demand and restricted supply in 2009.” However, Fleming, added, “How these government supports are removed in 2010 and the moderation of pending inventory and negative equity will be critical to the continued stability of the housing market.”

Treasury Policy Change

By Kenneth R. Harney, Realty Times

The Obama administration announced a blockbuster policy change over the holidays that didn't get a lot of press attention, but will affect the housing market for years.

The Treasury department said it is now committed to support Fannie Mae and Freddie Mac with as many billions of dollars as is necessary to get them through the next three years. There'll be no limit whatsoever anymore.

Previously the Treasury had limited its support to $200 billion apiece for the two formerly-private, now government-controlled, mortgage finance giants.

From here on, the Treasury said in its policy announcement, there will no “uncertainty about the (government's) commitment to support the firms as they continue to play a vital role in the housing market during the current crisis.”

Though some critics howled that the Obama administration is writing a blank check, the significance of the move for real estate is potentially huge, for several reasons.

Number one: Fannie and Freddie provide funding for well over half the U.S. mortgage market -- making home sales and purchases possible for hundreds of thousands of consumers.

Number two: The fact that the two companies have an explicit, full faith and credit backstop from the U.S. Treasury means that Fannie and Freddie can borrow in the capital markets at more favorable rates. Those lower costs of capital can then be passed along - at least in part - to home loan borrowers in the form of lower interest rates.

Finally, a key reason for the policy change - which also included permission for the firms to retain larger mortgage-asset portfolios - is to help Fannie and Freddie provide deeper loan modification assistance to greater numbers of seriously troubled borrowers.

Both companies are now expected to reach out and offer loan principal forgiveness to delinquent and underwater home owners - something that the current Obama loan modification program does not permit.

Partly as a result, Obama's “Home Affordable Modification Program,” or “HAMP,” has been only minimally successful in attracting the participation of borrowers in the deepest trouble - especially those so far behind and underwater that they are walking away from their houses, sending back the keys to their lenders - and ultimately losses to Fannie and Freddie.

If the revised policy helps keep larger numbers of home owners out of foreclosure and out of walkaway mode, the impact on local real estate markets and home values could be significant over the coming couple of years.

The Obama administration announced a blockbuster policy change over the holidays that didn't get a lot of press attention, but will affect the housing market for years.

The Treasury department said it is now committed to support Fannie Mae and Freddie Mac with as many billions of dollars as is necessary to get them through the next three years. There'll be no limit whatsoever anymore.

Previously the Treasury had limited its support to $200 billion apiece for the two formerly-private, now government-controlled, mortgage finance giants.

From here on, the Treasury said in its policy announcement, there will no “uncertainty about the (government's) commitment to support the firms as they continue to play a vital role in the housing market during the current crisis.”

Though some critics howled that the Obama administration is writing a blank check, the significance of the move for real estate is potentially huge, for several reasons.

Number one: Fannie and Freddie provide funding for well over half the U.S. mortgage market -- making home sales and purchases possible for hundreds of thousands of consumers.

Number two: The fact that the two companies have an explicit, full faith and credit backstop from the U.S. Treasury means that Fannie and Freddie can borrow in the capital markets at more favorable rates. Those lower costs of capital can then be passed along - at least in part - to home loan borrowers in the form of lower interest rates.

Finally, a key reason for the policy change - which also included permission for the firms to retain larger mortgage-asset portfolios - is to help Fannie and Freddie provide deeper loan modification assistance to greater numbers of seriously troubled borrowers.

Both companies are now expected to reach out and offer loan principal forgiveness to delinquent and underwater home owners - something that the current Obama loan modification program does not permit.

Partly as a result, Obama's “Home Affordable Modification Program,” or “HAMP,” has been only minimally successful in attracting the participation of borrowers in the deepest trouble - especially those so far behind and underwater that they are walking away from their houses, sending back the keys to their lenders - and ultimately losses to Fannie and Freddie.

If the revised policy helps keep larger numbers of home owners out of foreclosure and out of walkaway mode, the impact on local real estate markets and home values could be significant over the coming couple of years.

Monday, October 26, 2009

Big Rebound in Existing-Home Sales Shows First-Time Buyer Momentum

October 26, 2009

Existing-home sales bounced back strongly in September with first-time buyers driving much of the activity, marking five gains in the past six months, according to the National Association of Realtors®. Existing-home sales–including single-family, townhomes, condominiums and co-ops–jumped 9.4% to a seasonally adjusted annual rate of 5.57 million units in September from a level of 5.10 million in August, and are 9.2% higher than the 5.10 million-unit pace in September 2008. Sales activity is at the highest level in over two years, since it hit 5.73 million in July 2007.

Lawrence Yun, NAR chief economist, said favorable conditions matched with a tax credit are boosting home sales. “Much of the momentum is from people responding to the first-time buyer tax credit, which is freeing many sellers to make a trade and buy another home,” he said. “We are hopeful the tax credit will be extended and possibly expanded to more buyers, at least through the middle of next year, because the rising sales momentum needs to continue for a few additional quarters until we reach a point of a self-sustaining recovery.”

Even with the improvement, Yun said the market is underperforming. “Despite spectacular gains in the stock market, principally from the financial sector recovery, most of the 75 million home owning families have more wealth tied to their homes. Home values could soon turn consistently positive and help the broad base of middle-class families, but we are not there yet,” he said. “We’re getting early indications of price stabilization, but we need a steady supply of qualified buyers to meaningfully bring inventories down and return us to a period of normal, steady price growth and to fully remove consumer fears, which would then revive the broader economy. Without a firm foundation for middle-class wealth recovery, the post-recession economic growth likely will be one of the weakest in U.S. history.”

Early information from a large annual consumer study to be released November 13, the 2009 National Association of Realtors® Profile of Home Buyers and Sellers, shows that first-time home buyers accounted for more than 45% of home sales during the past year. A separate practitioner survey shows that distressed homes accounted for 29% of transactions in September.

NAR President Charles McMillan, a broker with Coldwell Banker Residential Brokerage in Dallas-Fort Worth, said affordability conditions remain historically high. “Potential first-time buyers can take heart in that affordability conditions this year are the highest on record dating back to 1970, but with the first-time buyer tax credit scheduled to expire at the end of next month, people could hold back from entering the market,” he said. “Our read is that housing overshot on the downside because homes are selling for less than replacement construction costs in much of the country, and the home price-to-income ratio has fallen below the historical average,” McMillan said.

Total housing inventory at the end of September fell 7.5% to 3.63 million existing homes available for sale, which represents an 7.8-month supply at the current sales pace, down from an 9.3-month supply in August. Unsold inventory totals are 15.0% below a year ago.

“The current housing supply is the lowest we’ve seen in two and a half years,” Yun said. “If we could continue to absorb inventory at this pace, home prices would return to normal, modest appreciation patterns next year.

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to 5.06% in September from 5.19% in August; the rate was 6.04% in September 2008. The national median existing-home price for all housing types was $174,900 in September, which is 8.5% lower than September 2008. Distressed properties continue to downwardly distort the median price because they generally sell at a discount relative to traditional homes in the same area.

Single-family home sales rose 9.4% to a seasonally adjusted annual rate of 4.89 million in September from a pace of 4.47 million in August, and are 7.7% above the 4.54 million-unit level in September 2008. The median existing single-family home price was $174,900 in September, which is 8.1% below a year ago. Existing condominium and co-op sales jumped 9.7% to a seasonally adjusted annual rate of 680,000 units in September from 620,000 in August, and are 9.7% above the 561,000-unit pace a year ago. The median existing condo price was $175,100 in September, down 11.7% from September 2008.

Northeast

Regionally, existing-home sales in the Northeast increased 4.4% to an annual level of 950,000 in September, and are 11.8% higher than September 2008. The median price in the Northeast was $234,700, down 7.0% from a year ago.

Midwest

Existing-home sales in the Midwest jumped 9.6% in September to a pace of 1.25 million and are 7.8% above a year ago. The median price in the Midwest was $147,600, which is 1.0% below September 2008.

South

In the South, existing-home sales rose 9.0% to an annual level of 2.06 million in September and are 10.8% higher than September 2008. The median price in the South was $153,500, down 7.6% from a year ago.

West

Existing-home sales in the West surged 13.0% to an annual rate of 1.30 million in September and are 5.7% above a year ago. The median price in the West was $219,000, which is 15.0% below September 2008.

Read more: http://rismedia.com/2009-10-25/big-rebound-in-existing-home-sales-shows-first-time-buyer-momentum/#ixzz0V3VvWcJG

Written by: RISMEDIA, rismedia.com

Existing-home sales bounced back strongly in September with first-time buyers driving much of the activity, marking five gains in the past six months, according to the National Association of Realtors®. Existing-home sales–including single-family, townhomes, condominiums and co-ops–jumped 9.4% to a seasonally adjusted annual rate of 5.57 million units in September from a level of 5.10 million in August, and are 9.2% higher than the 5.10 million-unit pace in September 2008. Sales activity is at the highest level in over two years, since it hit 5.73 million in July 2007.

Lawrence Yun, NAR chief economist, said favorable conditions matched with a tax credit are boosting home sales. “Much of the momentum is from people responding to the first-time buyer tax credit, which is freeing many sellers to make a trade and buy another home,” he said. “We are hopeful the tax credit will be extended and possibly expanded to more buyers, at least through the middle of next year, because the rising sales momentum needs to continue for a few additional quarters until we reach a point of a self-sustaining recovery.”

Even with the improvement, Yun said the market is underperforming. “Despite spectacular gains in the stock market, principally from the financial sector recovery, most of the 75 million home owning families have more wealth tied to their homes. Home values could soon turn consistently positive and help the broad base of middle-class families, but we are not there yet,” he said. “We’re getting early indications of price stabilization, but we need a steady supply of qualified buyers to meaningfully bring inventories down and return us to a period of normal, steady price growth and to fully remove consumer fears, which would then revive the broader economy. Without a firm foundation for middle-class wealth recovery, the post-recession economic growth likely will be one of the weakest in U.S. history.”

Early information from a large annual consumer study to be released November 13, the 2009 National Association of Realtors® Profile of Home Buyers and Sellers, shows that first-time home buyers accounted for more than 45% of home sales during the past year. A separate practitioner survey shows that distressed homes accounted for 29% of transactions in September.

NAR President Charles McMillan, a broker with Coldwell Banker Residential Brokerage in Dallas-Fort Worth, said affordability conditions remain historically high. “Potential first-time buyers can take heart in that affordability conditions this year are the highest on record dating back to 1970, but with the first-time buyer tax credit scheduled to expire at the end of next month, people could hold back from entering the market,” he said. “Our read is that housing overshot on the downside because homes are selling for less than replacement construction costs in much of the country, and the home price-to-income ratio has fallen below the historical average,” McMillan said.

Total housing inventory at the end of September fell 7.5% to 3.63 million existing homes available for sale, which represents an 7.8-month supply at the current sales pace, down from an 9.3-month supply in August. Unsold inventory totals are 15.0% below a year ago.

“The current housing supply is the lowest we’ve seen in two and a half years,” Yun said. “If we could continue to absorb inventory at this pace, home prices would return to normal, modest appreciation patterns next year.

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to 5.06% in September from 5.19% in August; the rate was 6.04% in September 2008. The national median existing-home price for all housing types was $174,900 in September, which is 8.5% lower than September 2008. Distressed properties continue to downwardly distort the median price because they generally sell at a discount relative to traditional homes in the same area.

Single-family home sales rose 9.4% to a seasonally adjusted annual rate of 4.89 million in September from a pace of 4.47 million in August, and are 7.7% above the 4.54 million-unit level in September 2008. The median existing single-family home price was $174,900 in September, which is 8.1% below a year ago. Existing condominium and co-op sales jumped 9.7% to a seasonally adjusted annual rate of 680,000 units in September from 620,000 in August, and are 9.7% above the 561,000-unit pace a year ago. The median existing condo price was $175,100 in September, down 11.7% from September 2008.

Northeast

Regionally, existing-home sales in the Northeast increased 4.4% to an annual level of 950,000 in September, and are 11.8% higher than September 2008. The median price in the Northeast was $234,700, down 7.0% from a year ago.

Midwest

Existing-home sales in the Midwest jumped 9.6% in September to a pace of 1.25 million and are 7.8% above a year ago. The median price in the Midwest was $147,600, which is 1.0% below September 2008.

South

In the South, existing-home sales rose 9.0% to an annual level of 2.06 million in September and are 10.8% higher than September 2008. The median price in the South was $153,500, down 7.6% from a year ago.

West

Existing-home sales in the West surged 13.0% to an annual rate of 1.30 million in September and are 5.7% above a year ago. The median price in the West was $219,000, which is 15.0% below September 2008.

Read more: http://rismedia.com/2009-10-25/big-rebound-in-existing-home-sales-shows-first-time-buyer-momentum/#ixzz0V3VvWcJG

Written by: RISMEDIA, rismedia.com

Thursday, October 8, 2009

Pelosi says homebuyer credit may be extended

The first time homebuyer tax credit may be extended, and even expanded, according to House Speaker Nancy Pelosi.

The $8,000 credit is set to expire Dec. 1.

“Yes, there is under consideration whether we extend the first time homeowners credit,” Pelosi said at a news conference Thursday. “And the question is, would that be just first time homeowners or would you open it up to other purchasers of homes.”

The tax credit has been among incentives fueling a rise in housing sales this year. The National Association of Realtors, which last month called on Congress to extend the credit, says it has brought 1.2 million new buyers into the market.

The NAR estimates 350,000 of those buyers would not have purchased a home without the credit.

Several lawmakers, including U.S. Sen. Benjamin L. Cardin, D-Md., have called for a six month extension of the credit.

An estimated 40 percent of all homebuyers in 2009 are eligible for the credit.

Washington Business Journal - by Jeff Clabaugh Staff Reporter

Monday, September 28, 2009

Mortgage Rates Remain Low, Increasing Affordability

McLEAN, VA -- Freddie Mac (NYSE:FRE) today released the results of its Primary Mortgage Market Survey (PMMS) in which the 30-year fixed-rate mortgage (FRM) averaged 5.04 percent with an average 0.6 point for the week ending September 24, 2009, unchanged from last week when it averaged 5.04 percent. Last year at this time, the 30-year FRM averaged 6.09 percent.

The 15-year FRM this week averaged 4.46 percent with an average 0.6 point, down from last week when it averaged 4.47 percent. A year ago at this time, the 15-year FRM averaged 5.77 percent. This is the lowest the 15-year FRM has been since Freddie Mac started tracking it in 1991.

The five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 4.51 percent this week, with an average 0.5 point, unchanged from last week when it averaged 4.51 percent. A year ago, the 5-year ARM averaged 6.02 percent.

The one-year Treasury-indexed ARM averaged 4.52 percent this week with an average 0.6 point, down from last week when it averaged 4.58 percent. At this time last year, the 1-year ARM averaged 5.03 percent.

"Mortgage rates held relatively steady at three-month lows this week,” said Frank Nothaft, Freddie Mac vice president and chief economist. Correspondingly, the Mortgage Bankers Association reported that mortgage applications jumped 12.8 percent over the week of September 18th to the strongest pace since late May, boosted by refinancing activity."

"In its September 23rd policy statement, the Federal Reserve (Fed) indicated that it plans to keep its benchmark interest rate exceptionally low for an extended period. This will likely benefit consumers who opt for ARMs, because they are typically tied to shorter-term interest rates. The Fed also noted that activity in the economy and housing market has picked up and financial markets have improved.”

Published: September 25, 2009

Realtytimes.com

Tuesday, September 22, 2009

Real Estate Outlook: Recession is Over

Now it's official. The chairman of the Federal Reserve Board himself has said it publicly that it looks like the recession is over.

Here comes the recovery.

But there was a big footnote in Bernanke's speech on the economy last week in Washington: Don't look for a dramatic recovery.

It'll be more like a slow moving, plodding sort of improvement where the economy inches toward expansion. But there'll be no sudden, splashy return to economic boomtime anytime soon.

Bernanke's point about the end of the recession was underscored by a 2.7 percent jump in retail sales for the month of August, according to the Commerce Department.

That's an important indicator because the key to pumping up the economy again is to get consumers spending, and that appears to be happening. Not just for auto sales, which got a big boost in August from the government's "cash for clunkers" program, but also for other key categories, like food and clothing purchases, department store retail, entertainment and restaurant spending, sporting goods.

They were all up for the month, after having been mainly down for well over a year.

One reason for the pick-up in consumer spending: People feel more confident about the direction of the economy in the months ahead. They see the stock market up, so their retirement funds and 401 K plans are bouncing back.

They see home values stabilizing or growing in most areas, so their equity is beginning to increase again.

The one big negative -- and it's definitely a drag for housing -- is the unemployment rate, which Mr. Bernanke said won't be coming down fast, even with the end of the recession.

Nonetheless, the vast majority of Americans who do have jobs have seen their real wages rise this year, up five percent. That's the largest annual gain in fifty years.

All of this is feeding into the housing sector in key markets, such as southern California, where August sales were up 11 percent compared with the year before, according to MDA DataQuick. Even prices are rising slightly.

In the combined markets of Los Angeles, San Diego, Orange County, San Bernadino-Riverside and Ventura, the median price of homes sold gained 2.6 percent in August, which is very encouraging for one of the hardest-hit boom-to-bust areas of the country.

Meanwhile, the mortgage market continues to be exceptionally positive for housing sales and values: 30 year fixed rates averaged just above 5 percent last week, according to the Mortgage Bankers Association, and 15 year loans averaged 4.4 percent.

Published: September 22, 2009

by Kenneth R. Harney

RealtyTimes.com

Tuesday, September 1, 2009

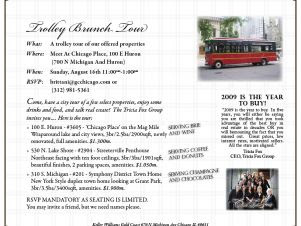

Terriffic Trolley Tours

Innovative Marketing

Tricia Fox has always done things a little bit differently from other real estate professionals in her downtown Chicago area. From art shows to shopping center kiosks to home-buying seminars that draw more than 500 people, Fox, broker of Tricia Fox Group of Keller Williams Luxury Real Estate in Chicago, does more than “take a listing, put it in the MLS, post it to a few websites and send out a postcard.”

So, when the weather turned cold, Fox decided to add luxury home tours by limo to her marketing repertoire. “Our offices are located on Michigan Avenue, and we specialize in properties in this area,” says Fox, who had 22 sales associates on her team and two staff members. The free limo tours took prospective buyers to several condominium listings in that area. But, it was so popular that Fox had to come up with a plan B. “We had such a great turnout that we decided to rent a trolley car so that we could seat more people,” she says. Fox recently took out her first trolley tour. “We had 32 seats, and they were all taken [15 couples]. Some of our team sales associates brought buyers on the tour, some sales associates waited at the properties,” she says. The group looked at seven resale properties and, according to Fox, three couples have taken a second look at some of the properties.

The trolley tours are free to prospective buyers and last about two hours. Each tour costs Fox about $1000 and she’s planning two a month. “Brunch is a good time of day for the tours,” says Fox.

Here are Fox’s tips for running a successful tour:

1. Plan ahead. The hardest part for Fox is the front-end planning. “You have to choose properties, make arrangements with owners [all properties are listed by Fox or someone on her team], decide who to invite and get the invitations out.” Fox has about 12 agents participate in the tours, so it’s vital to schedule several weeks in advance to ensure the entire group knows their assignments. “We have two agents at each site.”

2. Choose properties wisely. Fox only chooses vacant or sparsely furnished condos to show on the tour. “With so many people walking through the listing at once too much furniture makes it difficult,” she says. She also picks a price range for each tour. For example, one tour may feature lower-end properties that first time homebuyers or part-time residents may like; another tour might feature properties between $1 and $2 million. She then offers a mix of properties ranging from those with beautiful views to those with distinctive architecture.

3. Serve refreshments. Fox always serves refreshments at each property. “We may start with coffee at the first condo, then move on to wine and cheese. But, at the last property we always serve chocolates and champagne to make it festive,” she says.

4. Encourage conversation. Between properties, Fox visits in the trolley with each couple to answer questions. She also brings along a couple of mortgage brokers who can answer financing questions.

5. Use signs. Fox had some custom signs made that she can hang on the trolley for each tour. She also features brochures and signs at each listing.

6. Follow up. In addition to a feedback form she hands out, she has a follow up system for her team. “Individual agents follow up with the buyers and set up more appointments,” she says.

While she’s only done one tour, she’s learned a valuable lesson. “Next time, I would push people through the properties a little faster. We ended up with a lot of questions that could have been answered in the trolley on the way to the next property.”

It’s too soon to know exactly what kind of return on investment Fox will see. “Who knows what the actual return will be, but when you compare that cost to a print ad, the trolley is much more effective. It has the impact of personal touch. You can meet with people in person and really get to know them,” she says.

by Tracey Velt

Tricia Fox has always done things a little bit differently from other real estate professionals in her downtown Chicago area. From art shows to shopping center kiosks to home-buying seminars that draw more than 500 people, Fox, broker of Tricia Fox Group of Keller Williams Luxury Real Estate in Chicago, does more than “take a listing, put it in the MLS, post it to a few websites and send out a postcard.”

So, when the weather turned cold, Fox decided to add luxury home tours by limo to her marketing repertoire. “Our offices are located on Michigan Avenue, and we specialize in properties in this area,” says Fox, who had 22 sales associates on her team and two staff members. The free limo tours took prospective buyers to several condominium listings in that area. But, it was so popular that Fox had to come up with a plan B. “We had such a great turnout that we decided to rent a trolley car so that we could seat more people,” she says. Fox recently took out her first trolley tour. “We had 32 seats, and they were all taken [15 couples]. Some of our team sales associates brought buyers on the tour, some sales associates waited at the properties,” she says. The group looked at seven resale properties and, according to Fox, three couples have taken a second look at some of the properties.